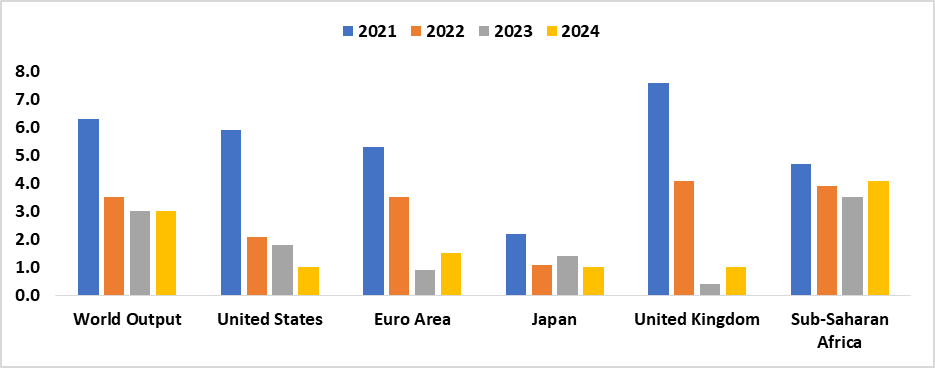

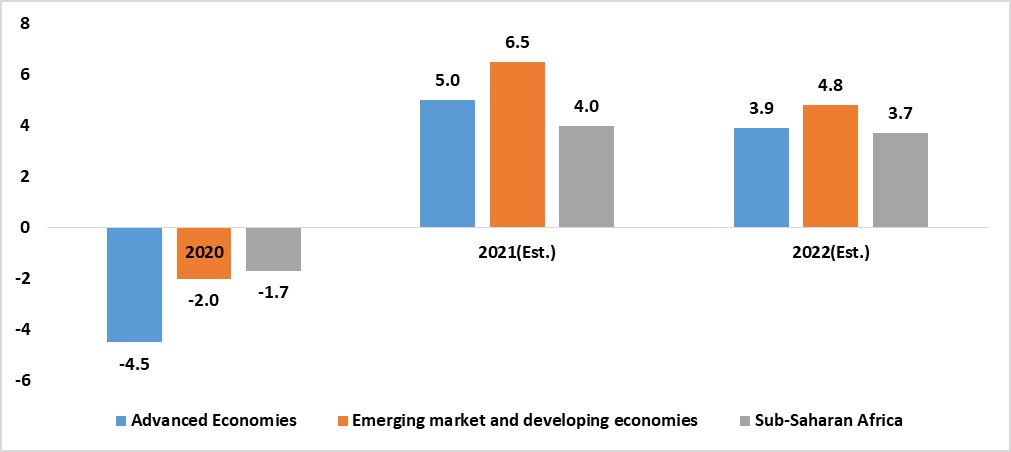

Global growth remains weak by historical standards. According to the recent World Economic Outlook published today, global growth is expected to slow from 3.5% in 2022 to 3.0% both in 2023 and 2024. The forecast for 2023 is slightly higher than predicted in the World Economic Outlook (WEO) for April 2023. The rise in central bank policy rates in order to combat inflation continues to have an impact on economic activity.

Growth in Sub-Saharan Africa is projected to decline to 3.5% in 2023 before picking up to 4.1% in 2024. Growth in Nigeria in 2023 and 2024 is projected to gradually decline, in line with April projections, reflecting security issues in the oil sector. In South Africa, growth is expected to decline to 0.3% in 2023, with the decline reflecting power shortages, although the forecast has been revised upward by 0.2% since the April 2023 WEO, on account of resilience in services activity in the first quarter. (Figure 1)

Additionally, global headline inflation is expected to fall from 8.7% in 2022 to 6.8% in 2023 and 5.2% in 2024. In 2023, roughly three-quarters of the world's economies are expected to have lower annual average headline inflation. Monetary policy tightening is expected to gradually dampen inflation, but falling international commodity prices are a key driver of the disinflation forecast for 2023. Differences in the rate of disinflation across countries reflect factors such as different exposures to commodity price and currency movements, as well as varying degrees of economic overheating.

Main forcesshaping the Global Outlook:

The fight against inflation continues. Inflation is easing in most countries but remains high, with divergences across economies and inflation measures

Acute stress in the banking sector has receded, but credit availability is tight. Thanks to the authorities’ swift reaction, the March 2023 banking scare remained contained and limited to problematic regional banks in the United States and Credit Suisse in Switzerland

Following a reopening boost, China’s recovery is losing steam. Manufacturing activity and consumption of services in China rebounded at the beginning of the year when Chinese authorities abandoned their strict lockdown policies; net exports contributed strongly to sequential growth in February and March as supply chains normalized and firms swiftly put backlogs of orders into production

Figure 1: Overview of the World Economic Outlook Projections (percentage change)

According to the World Bank Global Economic Prospectus of June 2023, the global economy is set to moderate to 2.1% in 2023 from a growth of 3.1% recorded in 2022, before a slight upturn of 2.4% in 2024. The global economy remains in a precarious state amid the protracted effects of the overlapping negative shocks of the pandemic, the Russian and Ukraine conflict, and the sharp tightening of monetary policy to contain high inflation. Inflation pressures persist, and tight monetary policy is expected to weigh substantially on activity in 2023. Recent banking sector stress in advanced economies will also likely dampen activity through more restrictive credit conditions. More widespread bank turmoil and tighter monetary policy could lead to even weaker global growth.

Growth in Sub-Saharan Africa is projected to slow to 3.2% in 2023, a 0.4% downward revision from January forecasts as external headwinds, persistent inflation, higher borrowing costs, and increased insecurity weigh on activity. Recoveries from the pandemic remain incomplete in many Sub-Saharan African countries, with elevated costs of living tempering the growth of consumption. Over half of the 2023 downgrade is attributable to an abrupt slowdown in South Africa. Growth in South Africa decelerated sharply in early 2023, reflecting policy tightening and the impact of an intensifying energy crisis.

South Africa

Despite concerns over load shedding and the potential impact on inflation and economic growth, the South African economy managed to avoid a technical recession. The South African economy recorded a rebound of 0.4% in economic activity during quarter 1 of 2023. Stats SA report indicated that the manufacturing and finance industries were the main drivers for economic growth during the period under review. The manufacturing sector demonstrated a modest growth rate of 1.5%, followed by the construction and the transport, storage, and communication sector, both experiencing growth rates of 1.1% respectively.

However, certain sectors faced challenges despite the overall economic recovery. Load shedding, in particular, hindered growth, leading to a significant decline of 12.3% in the agriculture, forestry, and fishing sector. Further to this, the excessive rainfall received at the beginning of the season resulted in difficult conditions for field crops, causing disruptions and delays in planting, with some areas experiencing delays of over a month. Additionally, the livestock sector continues to face challenges stemming from foot and mouth disease, leading to a decrease in slaughtering activity. Another significant sector that recorded a decline was the electricity, gas, and water sector. This decline was attributed to Eskom's current inability to generate sufficient electricity to meet demand. (Figures 1 & 3).

Namibia

The Namibian economy recorded a growth of 5.0% in the first quarter of 2023, a slower growth when compared to the 7.3% growth rate that was recorded in the corresponding quarter of 2022. The quarter-on-quarter decline in economic performance was largely attributed to contractions in the financial services which declined by 4.9%. Poor performance in the sector was attributed to both banking services and the insurance services subsectors as a result of the deterioration in the stock of net claims on central government and the decline in the real total deposits and claims. Additionally, the manufacturing sector also recorded the second notable decline of 2.7% during the period under review. The decline in the manufacturing sector activities was a result of the reduction in real value added in subsectors of grain mill, beverages, and dairy products which came as a result of low volume sales of grain mill products as well as the volume produced in the beverages sub-sectors.

Furthermore, the 'agriculture and forestry, health sectors also experienced significant declines of 3.6 %, 2.6% respectively. Low growth in the agriculture and forestry sector was attributed to low growth in the crop farming subsector as a result of the adverse impact of inadequate, delayed, and erratic rainfall in the country. Poor performance in health could be attributed to a deceleration in real compensation for employees.

Additionally, sectors such as mining and quarrying and ‘electricity and water’ posted growths. The sectors contributed 3.7% and 0.5% to GDP during the period under review. Furthermore, activities also picked up in the sectors of administrative and support services, transport and storage, wholesale and retail trade, and hotels and restaurants (Figures 2 & 3).

Undoubtedly, Namibia's economic structure bears a striking resemblance to that of South Africa, particularly in terms of the sectors that make significant contributions to both countries' Gross Domestic Product (GDP). Namibia and South Africa exhibit similarities in their economic structures, particularly in the significance of the mining and quarrying sectors, which contribute substantially to their exports and employment. Both countries possess abundant mineral resources like diamonds, gold, and uranium. Furthermore, agriculture holds importance for both economies, though South Africa has a more prominent agricultural industry due to a larger share of cultivable land. Additionally, Namibia's coastal location enables a strong focus on the fishing sector, contributing significantly to its GDP and export revenue. Namibia has also experienced double-digit growth in the manufacturing sector and hence, diversifying its economy away from the dependence on raw materials from the primary sector. In contrast, South Africa's economy is more diversified, with a well-developed industrial sector and a prominent financial and services industry. Overall, these similarities and differences shape the economic landscapes of Namibia and South Africa (Figures 4&5).

Figure 1: South Africa’s Key Industry growth rates- Q1 2023 compared with Q1 2022

Figure 3: South Africa’s Q1 GDP Vs Namibia’s Q1 GDP % change quarter-on-quarter

Source: StatsSA, NSA & HEI Research

Figure 4: South Africa’s historic quarterly GDP for the top 3 sectors at current prices (millions R)

Source: StatsSA & HEI Research

Figure 5: Namibia’s Historic quarterly GDP for the top 3 sectors at current prices (millions N$)

Source: NSA & HEI Research

Outlook

In anticipation of the potential recovery of the South African economy, several factors support this outlook. Firstly, the strengthening of the rand is contributing to positive sentiment, partially attributed to the reduction of power outages during the winter season, which aligns with historical production trends of the state-owned power utility, Eskom. Moreover, measures implemented by the government, such as load curtailment, expanding the diesel rebate to the food value chain, and the introduction of the Agro-Energy Fund; the fund is targeting to assist about 836 farmers with R2.5 billion. These initiatives are expected to facilitate the recovery of the agricultural sector in South Africa. Additionally, the decrease in the frequency of power outages is seen as encouraging news for the overall economy.

However, the South African economy faces risks that could impede growth in the second quarter and throughout 2023. These risks include insufficient and unreliable electricity supply, potential sharp increases in government debt interest rates, remaining on the Financial Action Task Force (FATF) greylist for an extended period, slow and unequal domestic growth, and the potential impact of the tightening of monetary policy to address high inflation. Moreover, the sluggish global economic outlook affecting Namibia's commodity demand and export revenue, uncertainties surrounding the Chinese economy and its effect on the demand for metal commodities, currency volatility leading to higher costs of key imports, concerns about being greylisted by the Financial Action Task Force (FATF), water supply interruptions impacting coastal mines, and below-average rainfall across the country paint are factors that could hinder growth for the Namibian economy in 2023, putting pressure on Namibian consumers and producers.

The domestic economy continued with resilience for the year 2022 from the devastating global economic shocks which included the effects of the Russian conflict with Ukraine and compounded the residual economic effects of the Covid-19 crisis, hindering growth and driving inflation to multi-high levels. Spiraling food and energy prices squeezed households around the world, and the tightening of monetary policy by the central bank to rein in inflation exerted further pressure on Namibian consumers and producers and the entire economy. The domestic economy recorded a growth of 4.6% in 2022 in real terms (GDP growth unadjusted for inflation). While GDP growth adjusted for inflation was 12.1% for 2022. This implies that inflation eroded Gross Domestic Product (GDP) growth by 7.5%.

In monetary terms, Real Gross Domestic Product (RGDP) increased to N$ 144.1 from N$ 137.8 recorded in 2021, while Nominal Gross Domestic Product (NGDP) increased to N$ 206.2 billion from N$ 183.9 billion recorded for 2021. Consumer spending accounted for 78.2%, government spending 23.2%, investment 17.4%, and net exports (18.7%) of total Nominal Gross Domestic Product (NGDP).

Economic activity improved significantly when compared to the growth of 3.5% recorded in 2021 (See figures 1 & 2). The improved performance was mainly driven by the primary and secondary industries which recorded growth rates of 12.9% and 3.3%, respectively. The Tertiary industries also recorded improved performance of 2.2% from a growth of 1.8% recorded in 2021. The main sectors that contributed to the expansion of the economy were manufacturing, electricity, water, and mining and quarrying (See figure 3).

Analysis

The mining and quarrying sector recorded a strong growth of 21.6% in 2022 when compared to a growth of 11% registered in 2021. The growth in the sector was ascribed to the diamond mining subsector which registered robust growth. During the period under review, the growth recorded for the diamond mining subsector was ascribed to an increase in diamond production driven by the Debmarine diamond production which accounted for 80% in 2022. Debmarine’s diamond production increased by 52% in relation to 2021 primarily due to the new purpose-built vessel, the MV Benguela Gem, inaugurated in March 2022. Additionally, the mining of metal ores observed marginal growth rates recording 0.5%

The manufacturing sector recorded a growth of 5.0% during the period under review when compared to a contraction of 1.2% registered in 2021. The strong performance resulted from diamond processing, meat processing, and other food products that posted strong growths of 33.7%, 11.6%, and 4.8%

The electricity and water sector registered a growth of 10.3% in 2022 when compared to a decline of 8.4% registered in 2021. The robust performance in the sector was attributed to the electricity subsector which recorded a growth of 17.5% which emanated from an increase in domestic production

The administrative and support services sector recorded a positive growth for the first time since 2016. The sector registered a growth of 3.9% during the period under review. The recovery in the sector came as a result of increased demand for administrative and support services such as security services, travel agencies activities, and car rentals due to the recovery of the tourism sector

The construction industry has been contracting since 2016; in 2022, the sector contracted by 16.4%, compared to a decline of 11.3% in 2021. The poor performance was reflected in the construction works for civil engineering and related services and buildings and related services.

The financial and insurance service activities sector rebounded to post a growth of 1.7% during 2022 at the back of a contraction of 5.1% recorded in 2021. The improved performance was primarily driven by the financial service activities subsector which grew by 2.4% due to an increase in interest income (fees, charges, and commission) stemming from increased interest rates coupled with the improved economic activities in the domestic economy.

Figure 1: Namibia annual GDP growth rates (2011 – 2022)

Figure 2: Real GDP growth rates for selected economies (2022)

Source: IMF World Economic Outlook & HEI RESEARCH

Figure 3: GDP growth rates per sector (2021 & 2022)

Source: NSA & HEI RESEARCH

Outlook

The increase in mining activities drove the growth of the primary sector present the country’s most resilient sector from a production and export revenue perspective. Value addition and beneficiation of the mining and other primary commodities remains a critical component to consider. This will help create job opportunities for a vast majority of unemployed youth.

Additionally, the necessary fiscal discipline and the implementation of policy priorities, backed by fiscal transparency have the potential to keep the domestic economy on an upward trajectory. More importantly, the country must strive for inclusive growth.

We project that there will be broader spill-over effects from China’s reopening including more favorable global financial conditions and increased trade with other countries including Namibia. However, a weaker external demand compounded by inflation, currency depreciation, a looming energy crisis, and other domestic headwinds including poor rainfall continues to shape economic developments.

The domestic economy recorded a slowdown in economic activity for the third quarter of 2022. Economic activity declined by 1.7% in relation to Quarter 2 of 2022 and by 1.3% when compared to the corresponding quarter of 2021. Slow growth was recorded for major segments of the economy, with the agriculture and forestry, fishing and processing on board, construction, financial activities, and public administration sectors recording no growth during quarter 3 of 2022. However, the mining and quarrying, manufacturing and wholesale, and retail trade sectors posted double-digit growth during the period under review.

Analysis

The domestic economy expanded by 4.3% during the third quarter of 2022, slow growth when compared to 5.6% recorded during the corresponding quarter of 2021. (See figure 1). The agriculture and forestry sectors declined to 14.2% from 10.8% in relation to quarter 3 of 2022. Poor performance for the sector emanated from the livestock farming subsector which contracted by 18.9% as a result of the low number of livestock marketed for exports due to the restrictive measures that were imposed by South Africa to curtail the spread of food and mouth disease within their borders. The fishing and fish processing on board sector registered a decline of 3.1% during the period under review when compared to a growth of 1.6% in the corresponding quarter of 2021. Poor performance in the sector was observed in the fish landings due to the reduction in Total Allowable Catches (TAC).

The construction and public administration sectors continue to remain under pressure contracting for the fifth consecutive quarter by 10% and 2.7% respectively. The financial services activities sector also declined by 4.7% when compared to a growth of 2.4% recorded in quarter 3 of 2021.

Growth in advanced economies is anticipated to slow from 2.5% in 2022 to 0.5% in January 2023. Slowdowns of this scale can foreshadow a global recession and this has a spillover effect on the domestic economy. Growth in emerging markets and developing economies including Namibia are also projected to fall from 3.8% in 2022 to 2.7% in 2023, reflecting significantly weaker external demand compounded by high inflation, currency depreciation, tighter financing conditions, and other domestic headwinds that will result in subdued economic activities.

Given the uncertainty of the anticipated “global recession,” the Namibian economic performance remains volatile.

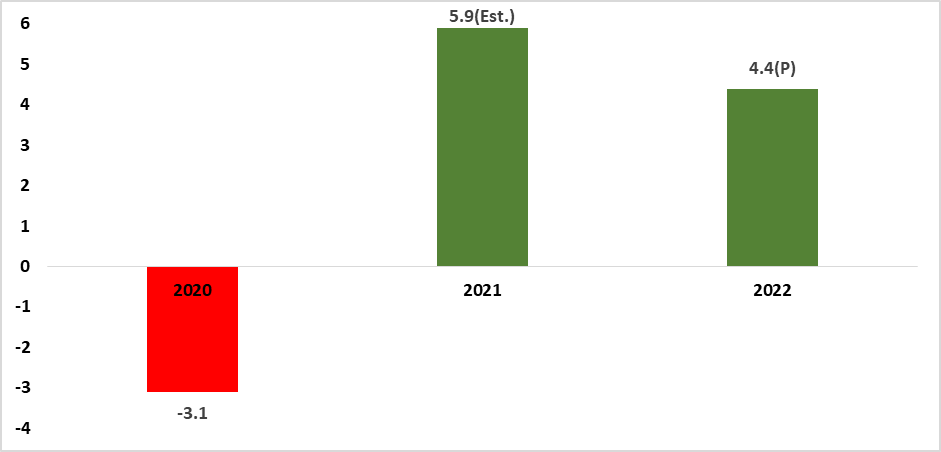

The Namibian economy showed signs of improvement in 2021 after the severe contraction recorded in 2020 due to the negative impact of the Covid-19 pandemic. The domestic economy recorded a recovery of 2.7% in 2021 from a contraction of 8.5% in 2020 (See figure 1 below). The domestic economy revision of 2.7% is an increase from the 2.4% that was recorded in the preliminary national accounts of 2021. The positive performance could be attributed to the relaxation of the restrictive measures that were imposed during the pandemic and a bounce in domestic economic activities. In monetary terms, Real Gross Domestic Product (RGDP) increased to N$ 136.7 billion from N$ 133.2 billion recorded for 2020. The primary and tertiary industries recorded a growth of 6.2% and 1.9% respectively while the secondary industries recorded a decline of 3.3%. The major sectors that attributed to the economy’s rebound were mining, and quarrying, hotels and restaurants, and transport (See figure 2). Namibian economic recovery continues to be driven by the tertiary sector followed by the secondary and primary sectors respectively. (See figure 3).

Analysis

The mining and quarrying sector registered a growth of 10% in 2021. The surge in the sector was mainly observed in uranium and other mining and quarrying subsectors. During the period under review, the growth recorded for the uranium subsector could be ascribed to an increase in uranium production that emanated from the high global demand for uranium ores. Additionally, growth in the other mining and quarrying subsectors was mainly due to the increase in the production of salt and marble

The hotels and restaurants sector registered a growth of 8.8% during the period under review, this was due to the relaxation of the Covid-19 travel and gathering restrictions, resulting in high demand for leisure, conferencing, and accommodation services

The wholesale and retail trade sector registered a growth of 6.1% as a result of an increase in the demand for vehicles, supermarkets, furniture, and wholesale outlets, the sector recorded the first ever growth since 2016

The health sector registered a growth of 4.3%. The positive performance emanated from an increase in the number of personnel and increased health expenditures

The professional, scientific, and technical services sectors registered a growth of 2.3%. The first positive performance since 2015. The recovery in the sector came as a result of the relaxation of strict pandemic measures coupled with improved tax compliance regulatory measures (taxpayers paying tax timely and accurately) that have propelled a resurgence in economic activities for the sector

The transport sector registered a growth of 2.2%. The main subsectors that contributed to the growth were air transport, airport services, port services, and freight transport by road which recorded positive growths of 14.8%, 30.0%, 5.7%, and 3.2%, respectively. This was influenced by an increase in aircraft movement, passenger arrivals, and cargo handled as a result of the easing of the Covid-19 travel restrictions and improved logistical chains

Figure 1: Annual GDP growth rates (2010 – 2021)

Source: NSA & HEI RESEARCH

Figure 2: GDP Growth per sector (2020 & 2021)

Source: NSA & HEI RESEARCH

Figure 3: Industries' contribution to GDP (2019 - 2021)

Source: NSA & HEI RESEARCH

Outlook

The growth of the Namibian economy is intertwined with the performance of the South African economy. South Africa’s GDP declined by 0.7% in quarter 2 of 2022 due to devastating floods in KwaZulu-Natal and continuous load shedding which had a negative impact on a number of industries, most notably manufacturing. As such Namibia’s GDP could be negatively affected as the country obtains most of its imports from South Africa. Hence, Namibia should strive and enhance its manufacturing industries to create more local enterprises. We anticipate a moderate recovery for the remaining of 2022 on the back of the anticipated recession in the advanced economies.

The economic fallout from the pandemic has had a severe impact on the Namibian economy leaving households and businesses vulnerable. The country’s Gross Domestic Product (GDP) improved since quarter 2 in 2021 as the Namibian economy is recovering from the pandemic due to related uncertainty and the “confluence of calamities” remains a concern. There are indications that consumption is gradually returning with a rebound in the Mining and Manufacturing activity.

The current rebound was mainly driven by the Agriculture and Forestry, and the Mining and Quarrying sectors.

The “organic “pace of recovery for domestic demand will be slowed by higher commodity prices and elevated uncertainty related to the Ukraine/Russian conflict. External demand will also be affected by the geopolitical tensions, mainly due to an expected slowdown in the advanced economies.

2. Analysis

The GDP recorded a rebound of 5.3% in the first quarter of 2022. The economic activity improved significantly from a decline of -4.9% during the same quarter last year. (See figure 1 below).

The rebound in the manufacturing sector of the country was driven by an increase in mining-related activities. The Agriculture and Forestry sector improvement was a result of normal to average rainfall received in 2021 and 2022 which boosted crop yield. See figure 2. During the period under review, the Mining and Quarrying sector recorded the highest annual recovery from -19.1% to 23.5% followed by the Manufacturing sector from -18.1% to 7.5%, Agriculture and Forestry sector from -2.9% to 5.9% in relation to the same period last year. In addition, sectors that contributed to the rebound are Health with 8.9%, Information, and Communication with 4.8%, and Hotels and Restaurants with 4.4%.

The Construction sector (See figure 2) continues to remain under pressure and contracted by 7.5%, while the Fishing sector also declined by 2.0%. The fiscal consolidation led to Public Administration recording a decline of 2.8% for quarter 1 of 2021.

Growth in advanced economies is projected to sharply decelerate from 5.1% in 2021 to 2.6% in 2022, which is 1.2 percentage points below projections in January 2022. Growth is expected to further moderate to 2.2% in 2023, largely reflecting the further unwinding of the fiscal and monetary policy support provided during the pandemic.

The emerging markets and developing economies, growth is also projected to fall from 6.6% in 2021 to 3.4% in 2022, well below the annual average of 4.8% over 2011-2019.

The Namibian economy could now be on the recovery path and quarter 2 of 2022 would be the turning point as it would eliminate the base effect and be a measure of the highly anticipated “organic” growth.

As the world strives to bring Covid-19 under control, fiscal policy remains key to address the impacts of the still-evolving pandemic, which continues to be marked by uncertainty. In the last quarter of 2021 the Omicron variant was associated with the resurgence of the virus. The fiscal support, especially in advanced economies, and vaccination have saved countless lives and facilitated an economic rebound. The interplay between vaccines and the virus and its variants is among the factors contributing to elevated uncertainty going forward.

The IMF (2021) made the point that fiscal policy need to respond to these challenges and facilitate the transformation of the global economy to make it more productive, inclusive, green, and resilient to future health or other crises.

At the same time, it will be crucial to ensure transparency and accountability, plot a medium-term path to rebuilding fiscal buffers, and make progress toward the Sustainable Development Goals.

Global Outlook

Global growth is estimated at 5.9% in 2021 and is expected to moderate to 4.4% in 2022(See figure 3). The anticipated effects of mobility restrictions, border closures and health impacts from the spread of the Omicron variant. The countries impact could vary depending on population demographics, the severity of mobility restrictions, the impact of infections on labor supply, and the importance of travel retail sectors. These impediments are expected to weigh on growth in the first quarter of 2022. The negative impact is expected to fade starting in the second quarter, assuming that the global surge in Omicron infections abates and the virus does not mutate into new variants that require further mobility restrictions.

The rise in inflation is expected to persist for longer than envisioned with ongoing supply chain disruptions and high energy prices anticipated to continue in 2022. Assuming inflation expectations stay well anchored, inflation should gradually decrease as supply-demand imbalances wane in 2022 and monetary policy in major economies responds.

Sub-Saharan Africa

The sub-Saharan Africa will be the world’s slowest growing region in 2022. According to IMF, the region is projected to record a growth of 3.7% in 2022(see figure 4).The global economy improved more rapidly than expected in the second half of 2021, with spillovers to the region in the form of increased trade, higher commodity prices, and a resumption of capital inflows.

The height of the Covid-19 pandemic crisis led policy discussion to different phases of the pandemic: immediate actions to save lives and livelihoods; near-term initiatives to secure a recovery once the acute phase of the crisis had passed; and then longer-term measures to build a more resilient and sustainable economy. For sub-Saharan Africa, however, all these phases may overlap, leaving authorities in the position of trying to boost and rebuild their economies while simultaneously dealing with repeated outbreaks as they arise.

The South Africa’s economy declined by 7% in 2020. A better-than-expected fourth quarter prompted an upward revision for 2021 although this will likely be offset by the third Covid-19 wave, which peaked in the fourth quarter and led to the reintroduction of some containment measures. The net impact will be a growth rate of 1.7% in 2021. Looking ahead, authorities have embarked on an ambitious vaccination program, which could limit the risk of additional waves if implemented swiftly. However, the scarring effects of the crisis, rising inequality, chronic electricity shortages, and product and labor market rigidities will likely weigh on growth over the medium term, limiting the economy’s ability to take advantage of the improving global environment albeit at the back of the Omicron variant.

Namibia

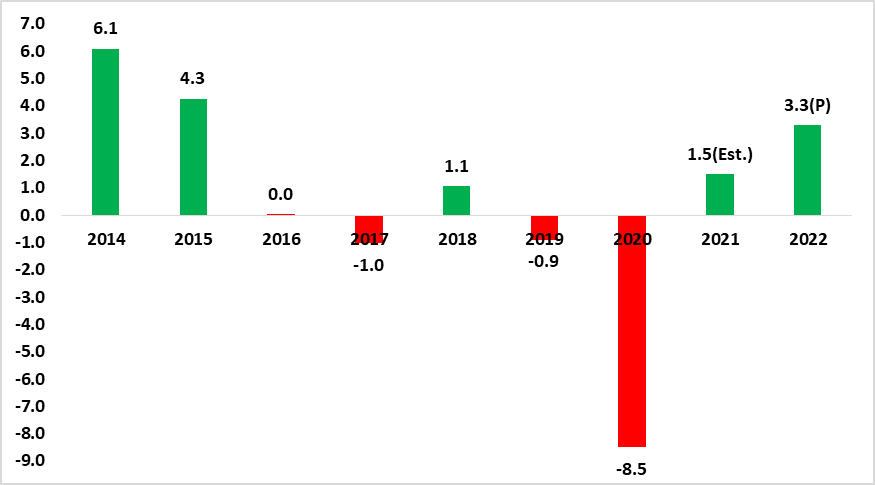

According to the Bank of Namibia, the domestic economy is projected to grow by 1.5% and by 3.3% in 2021 and 2022, respectively. This represents an improvement from 8.5% contraction recorded during the year 2020(See figure 2 below). The projected improvements are mainly due to base effects and better growth prospects for the mining industry and most of industries in the tertiary sector.

The Covid-19 pandemic is expected to remain a recovery and health risk going forward and therefore, fast recoveries in sectors that depend on travelling such as travel retail and accommodation are not expected in the short to medium term. Additional risks include an upsurge in the prices of goods and services locally. The Covid-19 pandemic has led to the monetary policy decision makers cutting the repo rate to its lowest levels of 3.75% with the aim to caution the ailing domestic economy due to the negative impact of Covid-19. This time around the policy makers could be left with no choice but to increase the rate further to control the rise in inflation.

During the year 2021 the Namibian economy recorded growth in the second and third quarters respectively, however this growth was derived from a very low base effects of the subdued economic activities in the year 2020. Namibia recorded growth in real gross domestic product in the second and third quarter of 2021, recording 1.6% and 2.4% growth respectively. The much anticipated growth in the economy in the second quarter of 2021 was observed across all sectors except for the agriculture and forestry, mining and quarrying, manufacturing, water and electricity, construction and financial services sectors. The positive growth in real GDP recorded during the third quarter of 2021 came from all the sectors with the exemption of construction, financial services, manufacturing and wholesale and retail trade sectors. Overall growth in real GDP for the third quarter of 2021 was mainly driven by growth recorded for the tertiary sector specifically the education and real estate and professional services activities sectors.

Outlook

According to IMF (2022) Sub-Saharan Africa economic region recorded a contraction of 1.7% in real economic output during the year 2020. This was due to the negative impact of the covid-19 pandemic. The economy for the Sub-Saharan Africa is estimated to grow by 4.0% for the year 2021 and grow by 3.7% in 2022 respectively. See figure 4 below.

On the domestic front, the global supply chain bottlenecks brought by the pandemic, high commodity prices, high inflation rate, subdued tourism industry, slow growth in the private sector credit extension and underwhelming rainfall received across the country paints a gloomy picture for the Namibian economy for the year 2022. Namibian consumers and producers could be under pressure and this will result in poor economic output for the year. Notwithstanding this, we anticipate for a minimal growth for the economy ranging between 1 and 2%. This growth is anticipated to be derived from very low base effects due to the continuous negative impact of the Covid-19 pandemic on the economy. The necessary fiscal discipline and clear communication of policy priorities, backed by fiscal transparency have the potential to reduce borrowing costs.

Figure

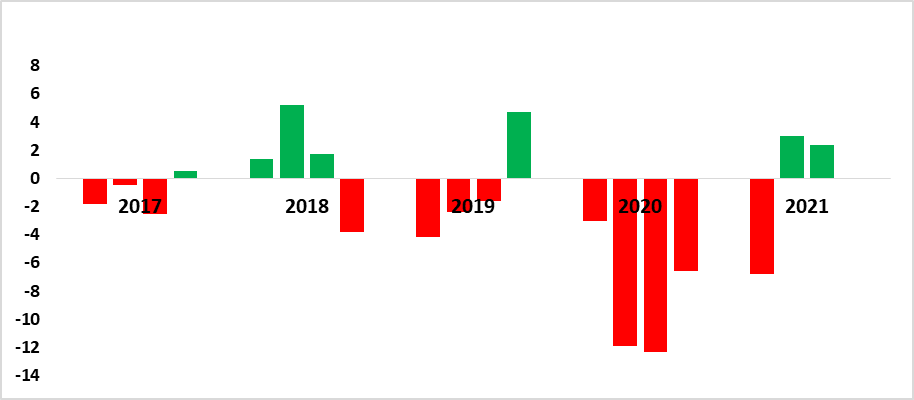

1: Quarterly real GDP growth rates, (2017-2021)

The Namibian economy was

hard hit during 2020 due to the negative impact of COVID-19 pandemic. The domestic

economy contracted by 8.5% during 2020 from a contraction of 0.9% recorded in

2019. Real Gross Domestic Product (RGDP) declined to N$ 132.5 billion from N$ 144.8 billion

recorded for 2019. This was the deepest economic contraction since

independence.

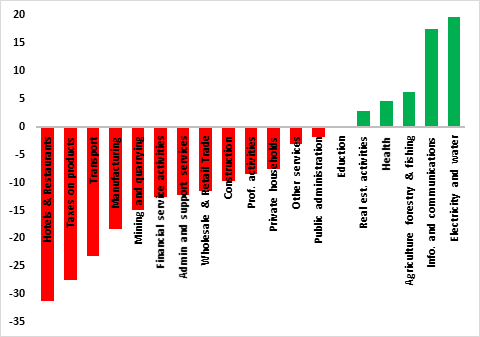

The main contributors to the economy’s contraction were the

manufacturing sector, taxes on products, mining and quarrying, wholesale and

retail trade and the financial services activities sectors. Out of a total of

18 sectors of the economy only 6 sectors registered growth for the year 2020

and the rest of the 12 sectors recorded a decline with the hotels and

restaurants sector leading the pack followed by the transport sector (See

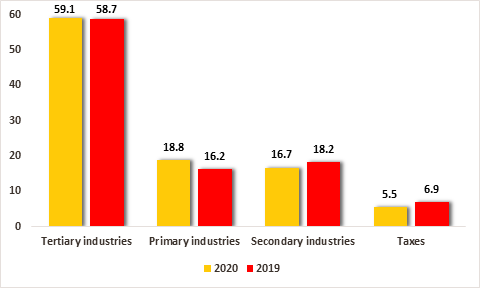

figure 1). The secondary industries recorded the greatest decline with 13.0%

followed by the tertiary industries with a decline of 5.7% and primary

industries contribution to GDP declined by 5.9%.

Namibia’s GDP is driven by the tertiary sector which was the main

contributor to the country’s economic growth. In a skills-constrained economy

like Namibia, the bias towards skills-intensive employment driven by

technological advancement has the unintended consequence of raising wage

premiums, which further entrenches inequality and contributes to rising

unemployment (See figure 2).

Analysis

The Hotels and the restaurants sector recorded the highest contraction

of 31.2% this was due to a lack of demand for accommodation services which

resulted from the lockdown restrictions imposed to contain the spread of

Covid-19 for the year 2020. The taxes on products sector recorded the second

highest contraction of 27.5%, this was due to reduced disposable income as a

result of retrenchments and job losses.

The transport sector recorded the third

highest contraction of 23.1%, this was due to the low demand for air transport

services as a result of local and international travel restrictions. The

manufacturing sector recorded the fourth largest contraction of 18.3%, this was

due to low production reported for processed zinc as a result of the closure of

the mine, low production of beverages as a result of the restriction on alcohol

sales and also a low production of meat (See figure 1).

The water and electricity sector recorded the highest growth of 19.5%,

this was driven by the growth in the electricity subsector due to good rainfall

received in the catchment areas. The information and communication sector

recorded the second highest growth of 17.4%, this was due to a high demand for

communication services. The agriculture forestry and fishing sector recorded

the third highest growth of 6.1%, this was driven by the growth in the crop

farming subsector as a result of good rainfall which resulted in good harvests

of cereal crops.

The health sector recorded the fourth largest growth of 4.5%,

this was driven by a high demand of health services due to Covid-19 (See figure

1 below). For the year 2020, the secondary industries recorded a decline of

13.0% from a growth of 2.2% recorded in 2019, this was driven by low growths

recorded in the manufacturing sector. The primary industries

recorded a decline of 5.9% from a decline of 6.9% recorded in 2019, the slight

growth was driven by the growth recorded

for the agriculture, forestry and fishing sector. Lastly the tertiary sector recorded a decline of 5.7%

from a growth of 1.1% recorded in 2019, this was driven by low growth recorded

in the transport sector, wholesale and retail sector and in the administrative

and support services (See figure 2 below).

Figure 1: GDP Growth per sector (2020)

Source: NSA & HEI RESEARCH

Figure 2: Industries contribution to GDP (2019 & 2020)

Source: NSA & HEI RESEARCH

Outlook

Economic prospects continue

to diverge across countries and vaccine access has emerged as the principal

fault line along which the global recovery deviates. The recovery, however, is

not assured even in countries where infections are currently very low so long

as the virus circulates elsewhere.

Economic policy has become

health policy and the efficient roll-out of Covid-19 vaccines will continue to

help flatten the curve. Additionally, the relaxed Covid-19 protocols gives an opportunity

for the economy to open up. However, an active demand of policies that caters

towards the rebuilding of the economy is highly advised.

Concerted,

well-directed structural

reforms can make the difference between a future of sustainable recovery for the Namibian economy or one with widening fault line, as many struggle with the health crisis while a

handful see conditions normalize, albeit with the constant threat of renewed

flare-ups

but to pre-covid19 levels.

The COVID-19 pandemic is in its second year

and concerns continue to rise about how

Namibia will recover from this. The Namibian economy has not responded very

well to the economic fallout from the pandemic with unprecedented downturns for

the hard-hit sectors and households. The

reality is that in the global economy some countries are rebounding faster than

others and uncertainty is high regarding the pandemic, especially in relation

to security of supply for the vaccines in the developing economies. This

requires that Namibia need to navigate a shifting landscape, in order to reset

the economy and achieve a sustainable recovery.

There are divergent recoveries in emerging markets

which reflect differences in economic positions and policy responses. Those

that were able to contain the virus or inoculate their populations[1]

are recovering earlier. Those with ample fiscal buffers, market access, or both

were able to deploy greater fiscal support[2].

In other countries Central bank credibility allowed some to cut policy rates to

record lows and engage in unconventional monetary policy by embarking on asset

purchasing programmes. Some countries with macroeconomic imbalances or elevated

debt burdens continue to face serious challenges in whether to support recovery

and reducing imbalances. Namibia and South Africa falls in the latter.

2.Analysis

Over the past five years the primary sectors contributed 16.8% on average to GDP. Mining and quarrying sector contributed around 10% on average to GDP between 2016 and 2020 on the back of very good performance of the mining and quarrying activities. Agriculture forestry and fishing sector contributed to 7.7% on average from 2016 until 2020 see figure 2. Agriculture reached its peak in 2020 and contributed 9% to GDP ,which was attributed to the good rainfall received and the bumper harvest for cereal crops.

Figure 1:Sectoral percentage contribution to GDP (2016-2020)

Source: NSA & HEI RESEARCH

The performance of the secondary sectors were driven by the manufacturing sector contributing up to 12% on average to GDP between 2016 and 2020. Mining related manufacturing activities such as manufacturing of basic zinc and diamond cutting and polishing, makes up the Namibian manufacturing sector and its contribution to GDP. Electricity and water sectors made up the second highest contribution for the secondary sectors to GDP. However, the growth of the secondary sectors and its contribution to the country’s GDP is hindered by the lack of investment in the sector which contribute to the lack of skills needed to increase production capacity and value addition.

Namibia’s GDP is driven by the tertiary sectors, and

between 2016 till 2020 the services sectors were the main contributors to the country’s

economic growth. In a

skills-constrained economy like Namibia, the bias towards skills-intensive

employment driven by technological advancement has the unintended consequence

of raising wage premiums, which further entrenches inequality and contributes

to rising unemployment.

The Namibian economy contracted for 5 consecutive quarters since 2020 with a deepest contraction recorded in third quarter of 2020 see figure 2. The year 2020 the economy declined by -7.9% on average. During the first quarter of 2021 the economy declined by -6.5% with the highest declines recorded for the construction sector ,manufacturing sector and mining and quarrying sector.

Figure 2 : GDP Growth rates (2016-2021)

Source: NSA

Outlook

The road ahead could be somewhat bumpy for Namibia

because of the threats from the mutation of COVID-19 strains as it continues

the spread with very little economic support to households and firms. There is

a need for normalizing policies and rebuilding economic resilience. Securing

adequate vaccines is a necessity and priorities will vary from country to

country.

Recommendations

Introduce measures through policies such as improved

insolvency and restructuring procedures

Promote

competition to enable the exit and entry of firms to help curb market power

Build local capacity for

domestic market for inward linkages (agriculture sector)

Supporting displaced workers, by gradually

refocusing policy support from retention to

reallocation

Ensuring adequate access to financing for viable companies