The decline in airport arrivals during September 2023 reflects a concerning trend in Namibia's tourism industry. The reduction in domestic and regional arrivals highlights the impact of rising living costs due to inflation. This financial strain led to a decline in travelers' confidence, prompting a cautious approach towards travel expenditures. The data underscores the need for strategic interventions and policies to bolster domestic and regional tourism, focusing on affordability and consumer confidence to revive the tourism sector and stimulate overall economic growth.

Analysis

In September 2023, total airport arrivals decreased to 39,921, down from the 42,518 arrivals recorded in August 2023, marking a 24.1% monthly decline (Figures 1 & 2). This decline was primarily due to an 18% decrease in domestic arrivals, followed by a 5% decline in regional airport arrivals (Figure 3). The reduction in domestic and regional travelers' confidence was linked to a high cost of living caused by a monthly increase in the inflation rate, leading to cautious spending on travel activities. Despite this, international arrivals accounted for 47.7% of the total arrivals in September 2023, with regional arrivals making up 39.5%, and domestic arrivals contributing to the remaining 12.7%.

On an annual basis, total airport arrivals experienced a significant decline of 52.7%. This decrease can be attributed to weakened travelers' confidence resulting from subdued consumer consumption patterns (Figure 4).

Figure 1: Monthly HKIA Arrivals September 2022 – September 2023)

Source: NAC &HEI RESEARCH

Figure 2: Year on Year % changes HKIA Arrivals (September 2022 – September 2023)

Source: NAC & HEI RESEARCH

Figure 3: Total International, Regional vs. Domestic Arrivals (September 2022 – September 2023)

Source: NAC & HEI RESEARCH

Figure 4: Month on Month % changes HKIA Arrivals (September 2022 – September 2023)

Source: NAC & HEI RESEARCH

Outlook

As the country approaches the festive season, with holiday packages and specials and the officially launched online tourist visa application service by the Ministry of Home Affairs, immigration, safety and security that allows travelers across the world to apply for tourist or holiday visas to Namibia from the comfort of their homes. We anticipate arrivals to increase in the short to medium term.

Between August and September 2023, credit extended to households and businesses in the private sector decreased by N$345.1 million. In real terms, total credit extended to the private sector decreased from N$119,288.8 million in August 2023 to N$118,943.7 million in September 2023. This decline was observed across all credit categories except for installment sales and leasing credit, which exhibited a modest increase of 11.6% during the period under review.

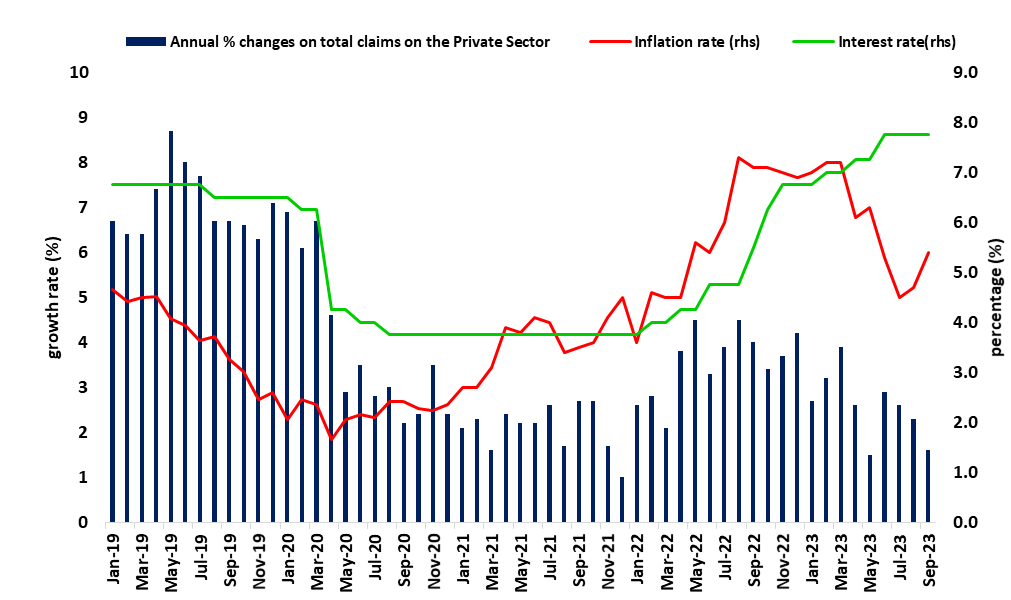

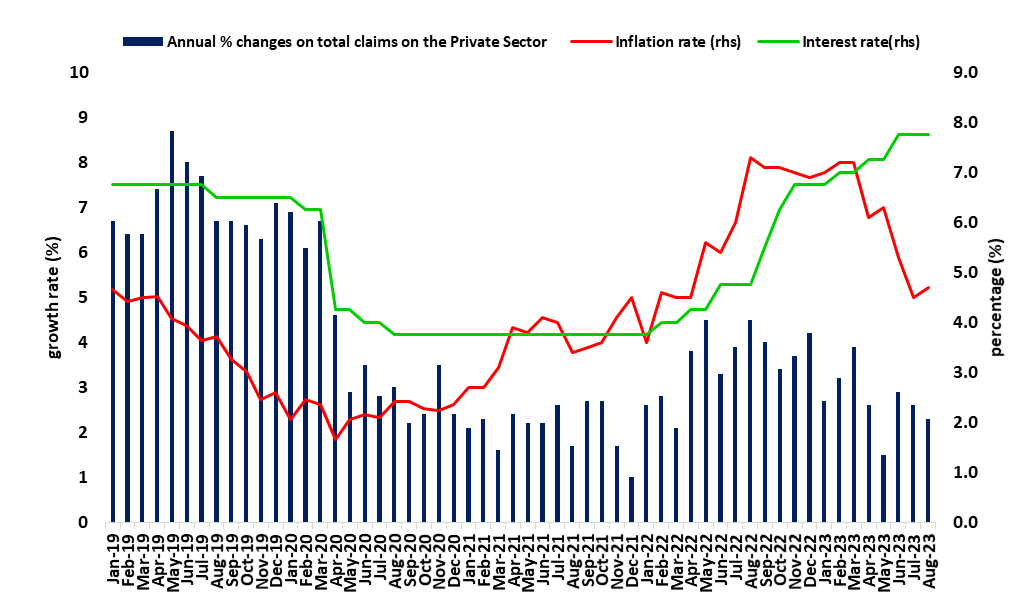

On an annual basis, the Private Sector Credit Extension (PSCE) recorded a growth rate of 1.6% a decline from the 2.2% growth rate recorded at the end of August 2023. This decline could be attributed to low demand for credit and the net repayment of credit by businesses, particularly in the services, wholesale, retail trade, commercial real estate, mining, manufacturing, and fishing sectors, as reported by the Bank of Namibia (see Figure 1). Moreover, business credit contracted by 2.1% year-on-year, while household credit experienced a decline of 4.3% year-on-year.

Figure 1: Annual % PSCE vs. Repo Rate & Interest Rate, (January 2019- September 2023)

Source: BON, NSA & HEI RESEARCH

Credit to Households

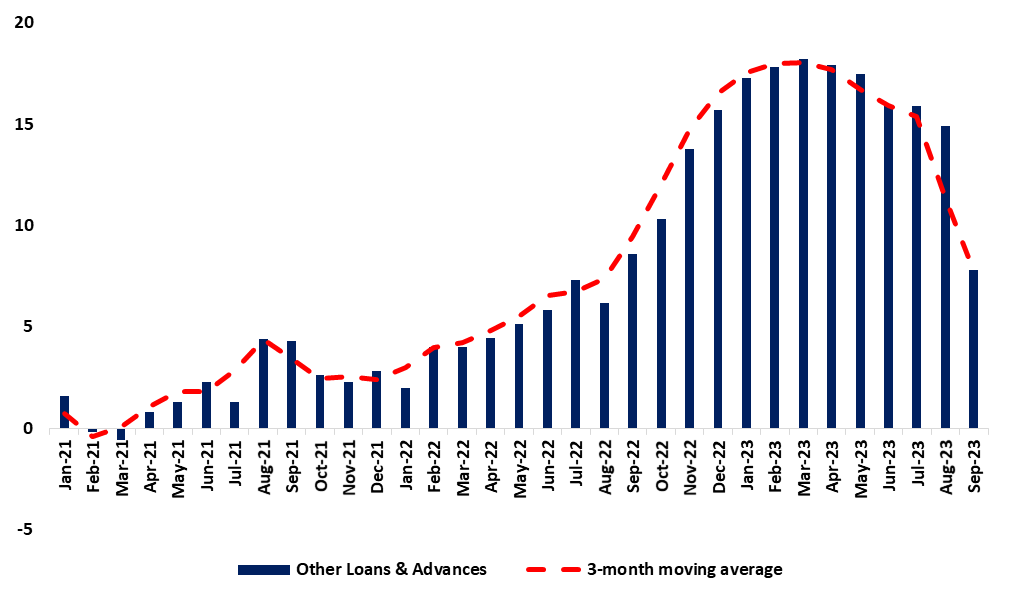

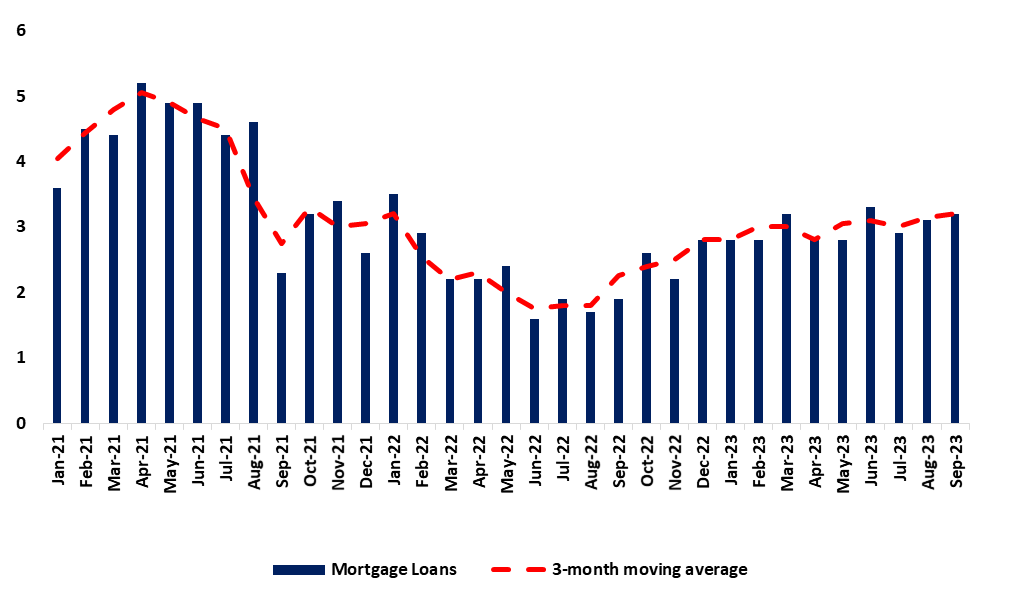

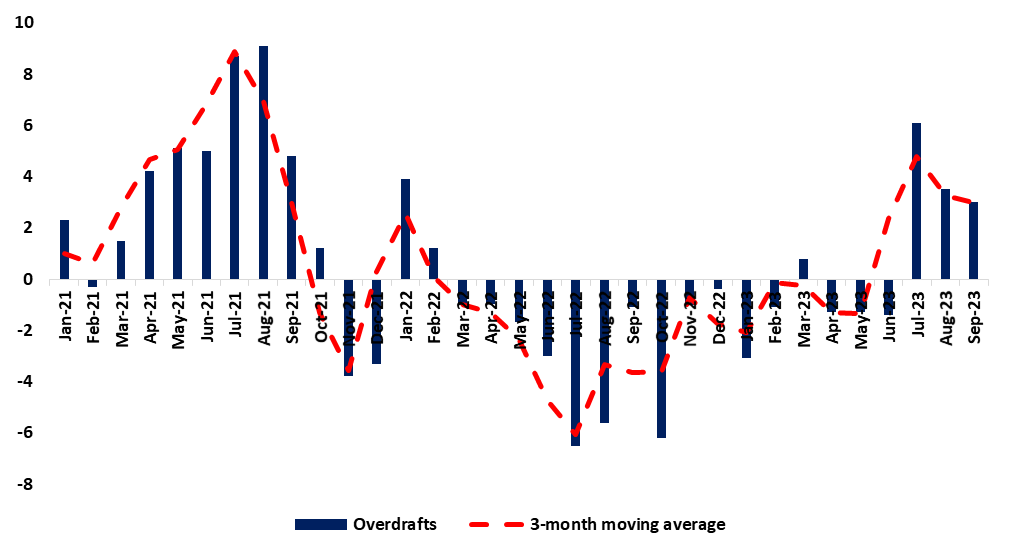

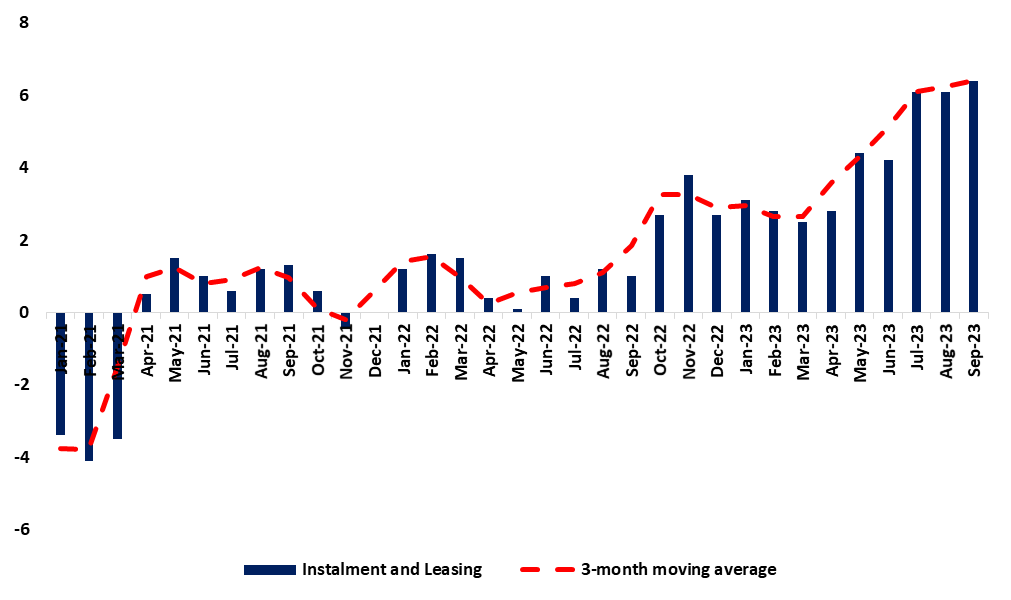

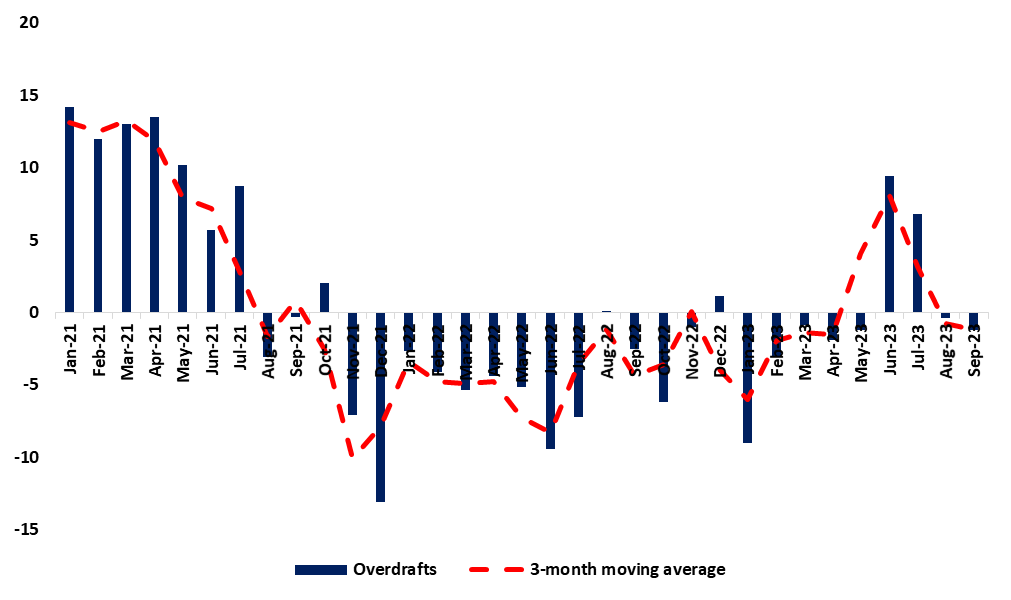

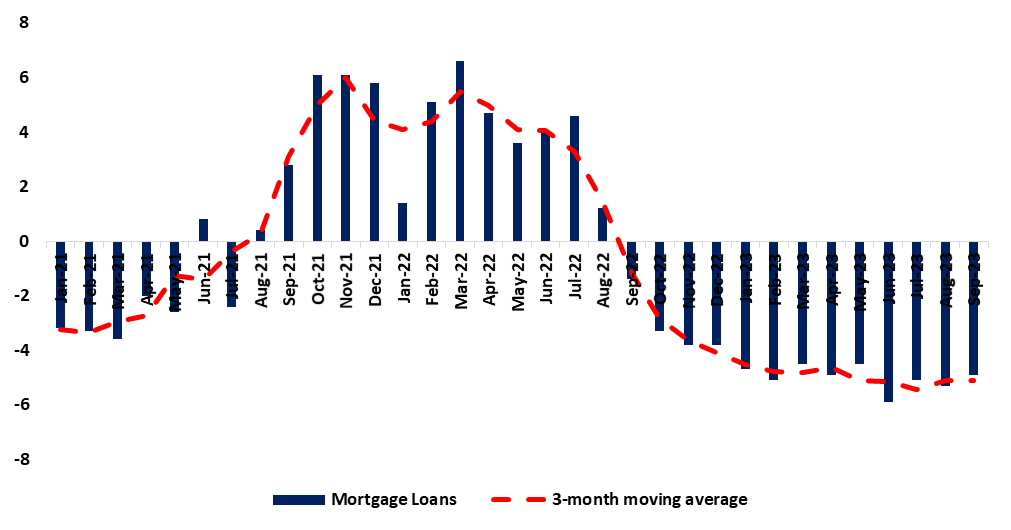

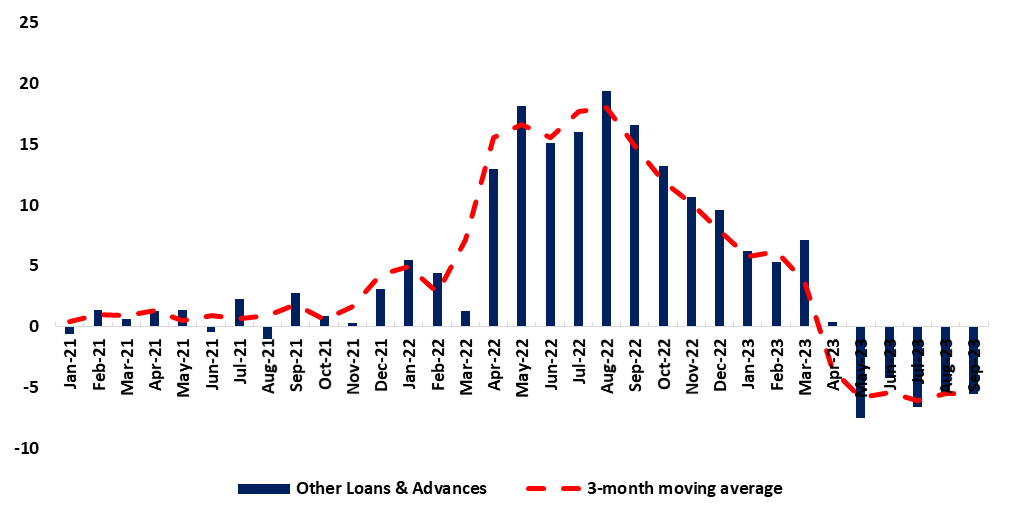

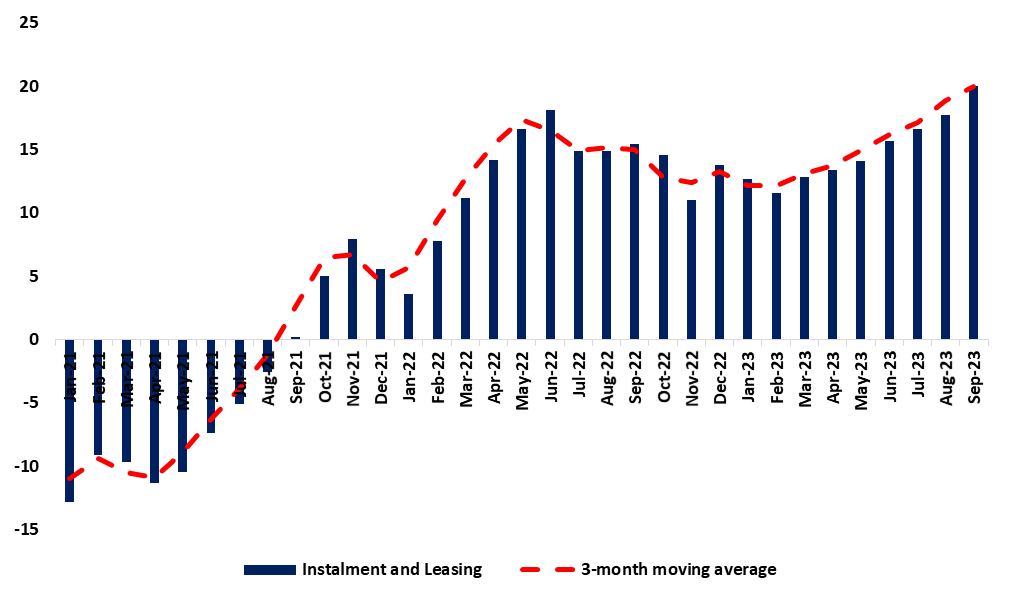

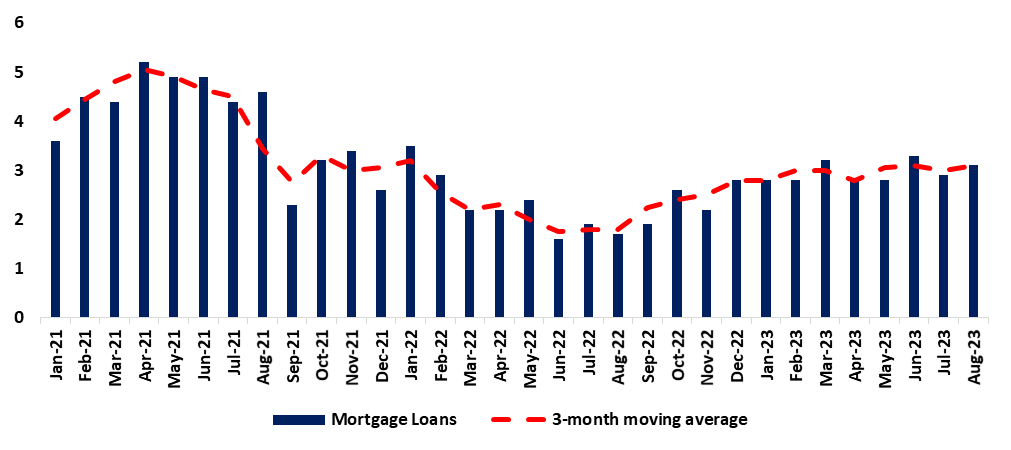

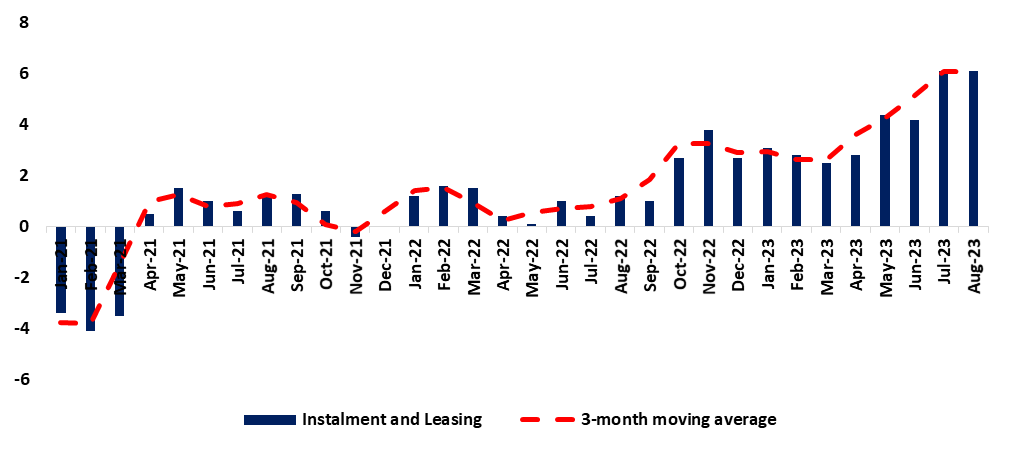

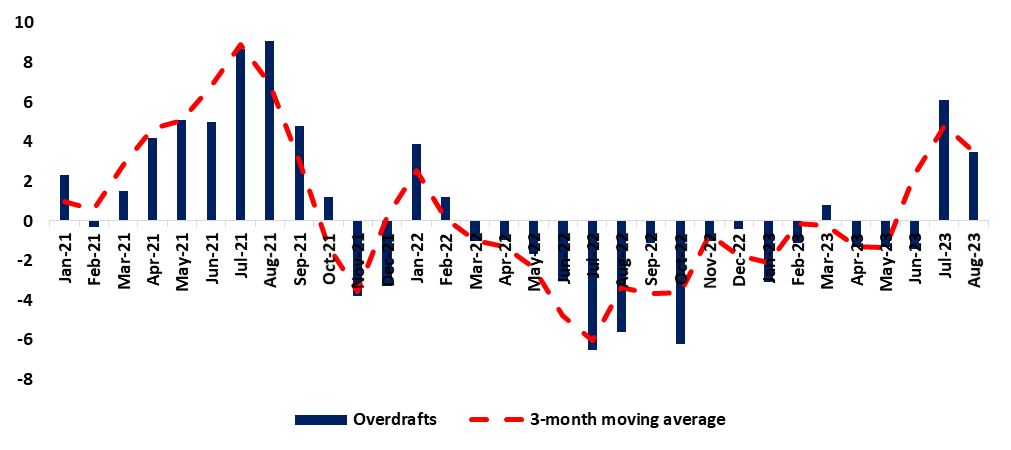

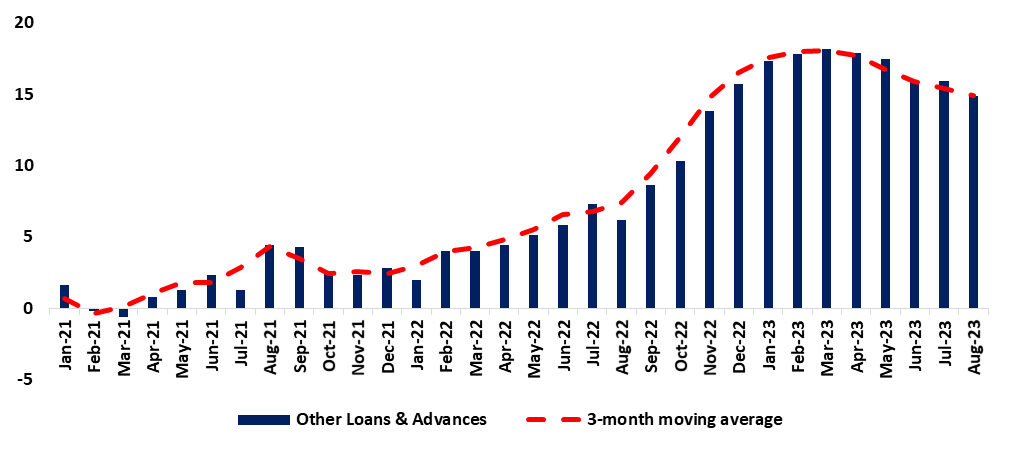

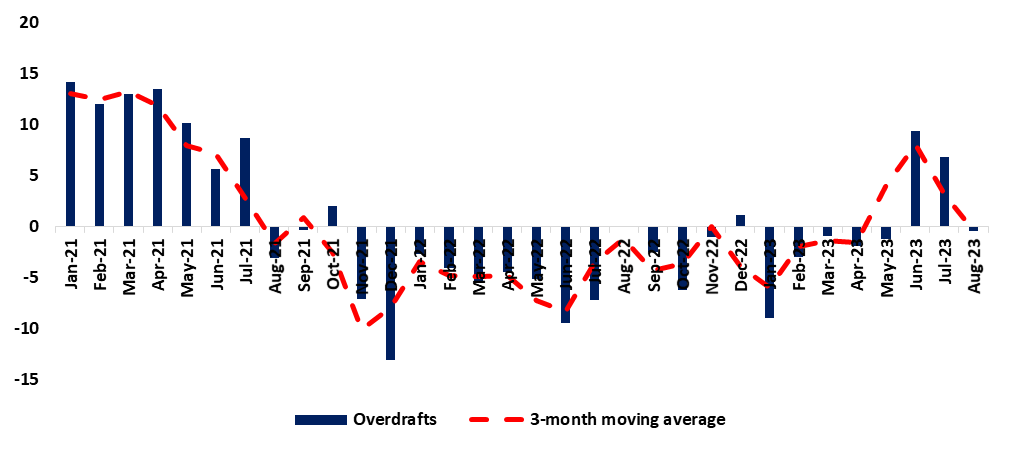

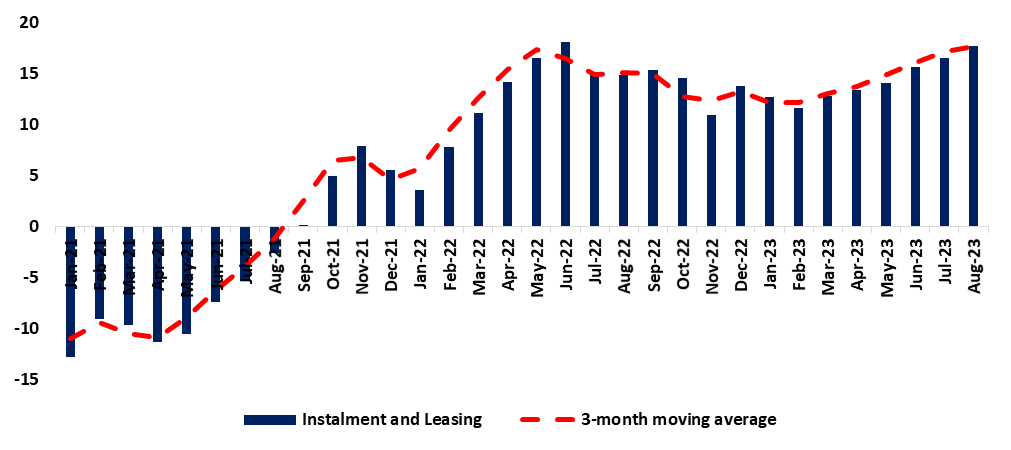

The credit extended to households stood at N$65,967.9 million in September 2023 from N$66,433 million in August 2023. This signified a weakening trend, primarily driven by sub-categories such as other loans and advances, which decreased from 14.9% to 7.8% month-on-month. In comparison, mortgage credit remained subdued at 3.2% month-on-month (refer to Figures 2 and 3). Consequently, most credit facilities available to households experienced declines, including overdraft credit, which decreased from 3.5% to 3.0%. However, there was a slight increase in installments and leasing credit, albeit modest, rising from 6.1% to 6.4% during the specified period (refer to Figures 4 and 5).

Figure 2: Other loans and advances, (January 2021- September 2023)

Source: BON, NSA & HEI RESEARCH

Figure 3: Mortgage, (January 2021- September 2023)

Source: BON, NSA & HEI RESEARCH

Figure 4: Overdrafts (January 2021- September 2023)

Source: BON, NSA & HEI RESEARCH

Figure 5: Instalments and Leasing, (January 2021- September 2023)

Source: BON, NSA & HEI RESEARCH

Credit to Businesses

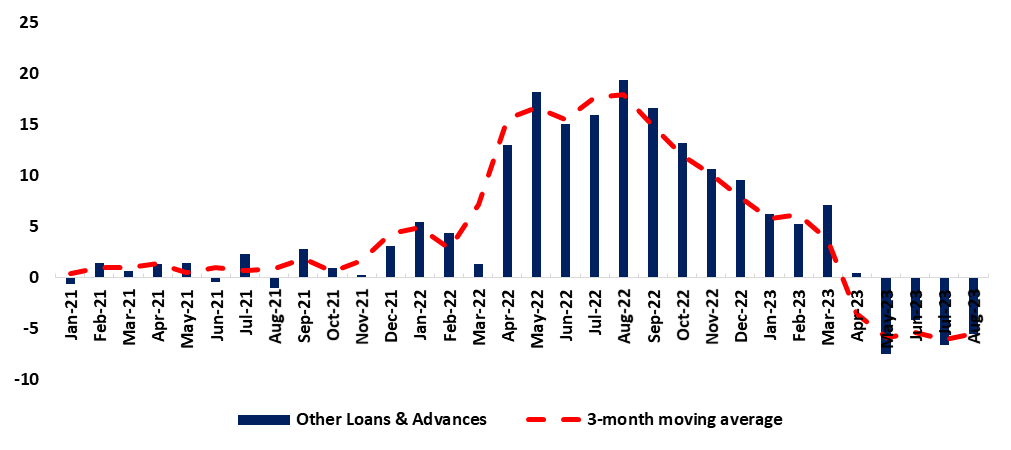

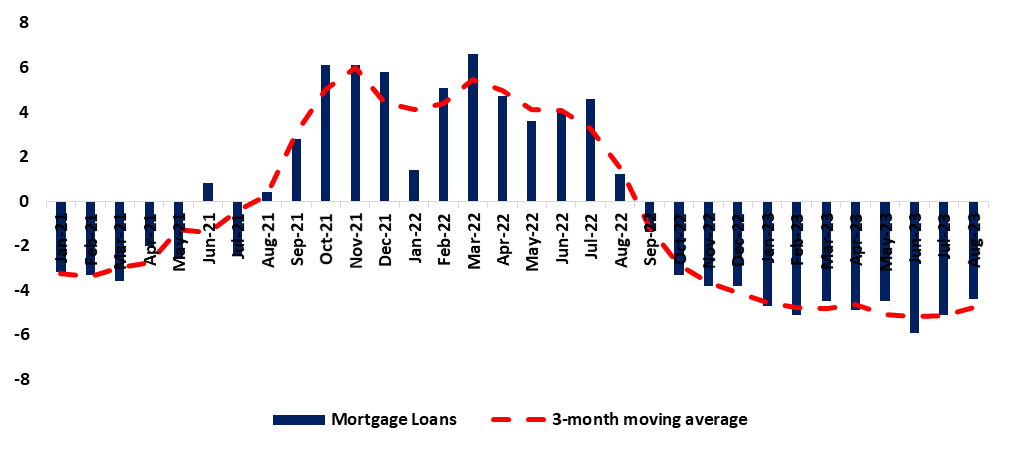

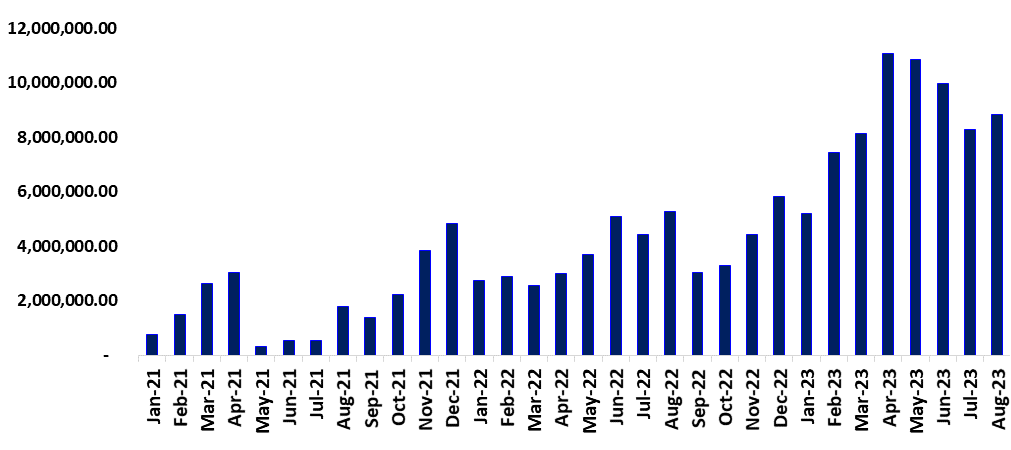

During the month under review (September 2023), total credit extended to businesses amounted to N$ 45,281 million, reflecting a marginal improvement from the August figure of N$ 45,188 million. This slight uptick was primarily driven by a surge in demand for installment and leasing credit, which increased from 17.8% to 20.0% month-on-month. This growth was spurred by heightened demand in the car rental industry, supported by activities within the tourism sector. On the other hand, overdraft credit experienced a decline, decreasing from 0.4% to -1.2% month-on-month, along with a contraction in mortgage loans, dropping from 5.3% to -4.9% month-on-month. Meanwhile, other loans and advances remained stable at -5.5%, as illustrated in Figures 6, 7, and 8 (refer to Figure 9).

Figure 6: Overdrafts, (January 2021- September 2023)

Source: BON, NSA & HEI RESEARCH

Figure 7: Mortgage, (January 2021- September 2023)

Source: BON, NSA & HEI RESEARCH

Figure 8: Other loans and advances, (January 2021- September 2023)

Source: BON, NSA & HEI RESEARCH

Figure 9: Instalments and Leasing, (January 2021- September 2023)

Source: BON, NSA & HEI RESEARCH

Commercial Bank Liquidity Position

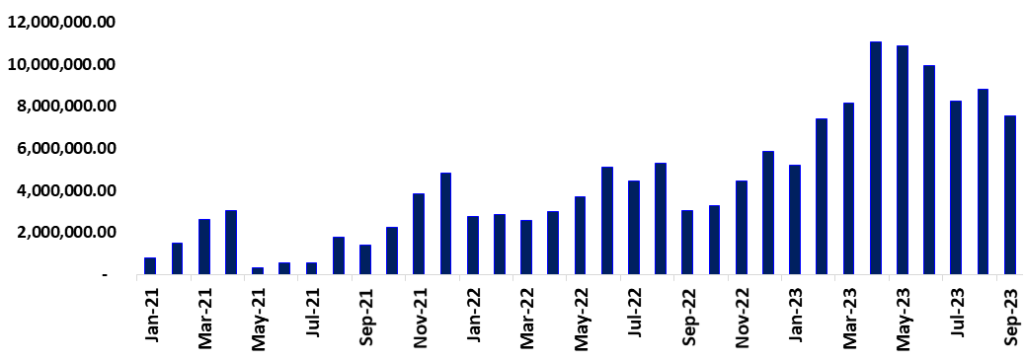

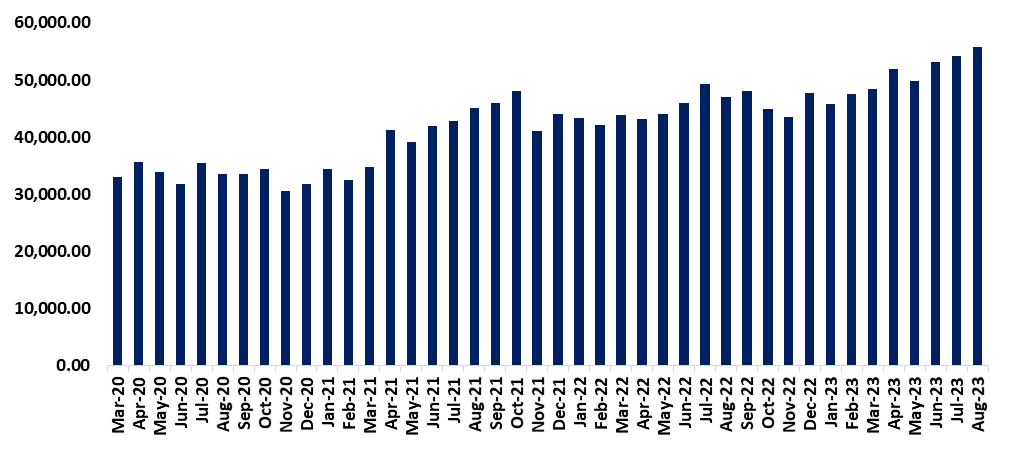

The aggregate liquidity status of the banking industry saw a decline to N$7.3 billion in September 2023, in comparison to the N$8.8 billion reported in August 2023, marking a month-on-month reduction of N$1.5 billion (see Figure 10). The Bank of Namibia (BoN) attributed this decline to factors such as reduced government expenditure, decreased diamond sales, and an increase in funds placed in the BoN Bill.

Figure 10: Banking Liquidity (January 2021- September 2023)

Source: BON, NSA & HEI RESEARCH

Foreign Reserves & Money Supply

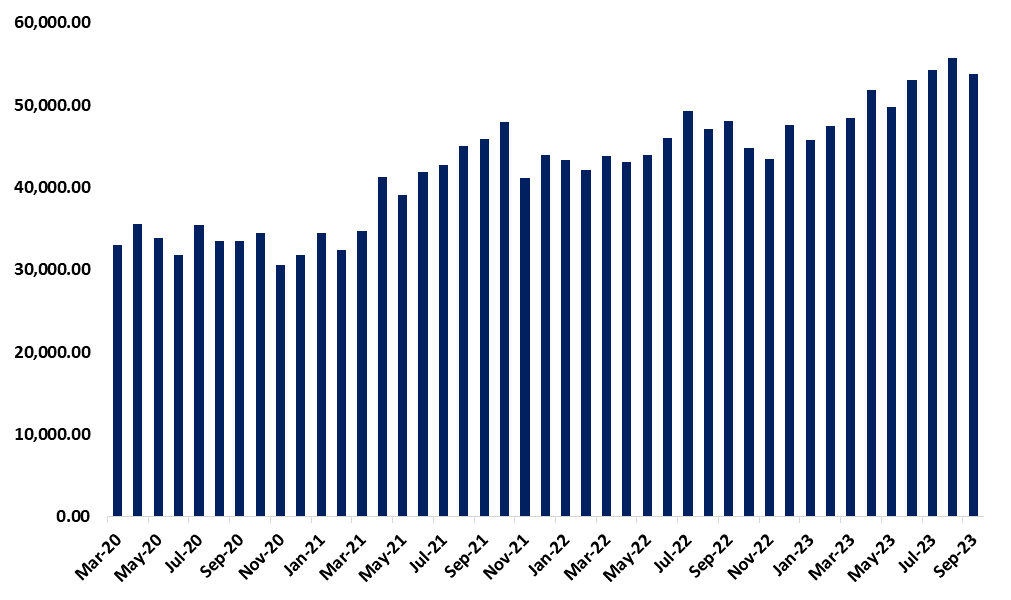

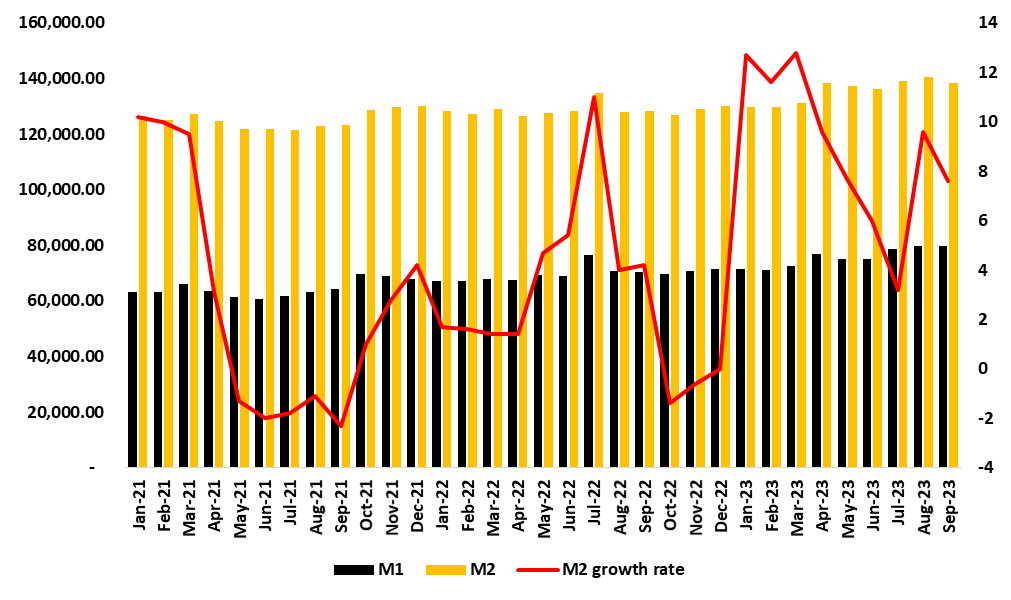

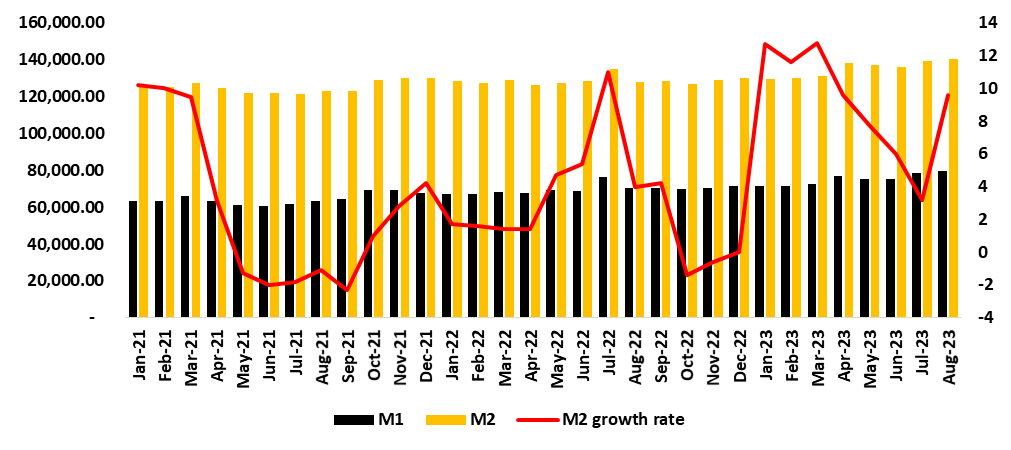

The Bank of Namibia saw a reduction in its stock of international reserves, which decreased from N$55.6 billion in August 2023 to N$53.8 billion in September 2023. This decline could be attributed to outflows from commercial banks and government payments, as illustrated in Figure 11. Due to these developments, the growth rate in broad money supply experienced a notable decrease, falling from 9.6% in August 2023 to 7.9% in September 2023, as shown in Figure 12.

Figure 11: Foreign Reserves (March 2020- September 2023)

The prevalence of homeownership facilitated by mortgages among households, along with the adoption of Installment and Leasing credit options by both households and businesses, often serves as an indicator of economic confidence and individual financial stability. Within Namibia's credit landscape, a subdued trend is distinct, evident in the restrained growth of various credit options such as overdrafts and other loans and advances available to households and businesses, coupled with constraints in liquidity.

Our analysis suggests that the trajectory of credit allocation to households and businesses is likely to face continued limitations in the near-to-intermediate future. Additionally, there is evidence of evolving preferences among households and businesses regarding the types of credit facilities they prefer, with a growing inclination towards installment and leasing options. It's worth noting that, with the central bank keeping the interest rates unchanged, consumers might experience some relief, particularly as they adjust to the effects of previous interest rate hikes.

The Bank of Namibia Monetary Policy Committee (MPC) is set to make its fifth announcement for 2023 regarding the interest rate decision tomorrow the 25th of October 2023. The MPC decided to keep rates unchanged at their last meeting in August 2023. That was their second unchanged MPC meeting. The repo rate currently stands at 7.75%, the highest it’s ever been in the past 14 years.

Additionally, inflation in Namibian currently stands at 5.4% from 4.7% recorded in August 2023. Inflation pressures remain elevated, driven by food and non-alcoholic beverages, and transport. Other countries in the CMA continue to lag behind South Africa's repo rate of 8.25% and a real interest rate of 2.85%. The South Africa Reserve Bank kept its repo rate unchanged at 8.25% in its last meeting held in September 2023. This results in a spread of 50 basis points between Namibia and South Africa's repo rates (Figure 1).

Core inflation in South Africa fell to 4.5% from 4.8% and Namibia remains unchanged at 4.9%, after months of raising prices in core components. This indicates subdued overall price pressures, providing a rationale for central banks to keep interest rates unchanged as a measure to stimulate spending and investment, supporting economic growth.

Figure 1: Repo and Interest Rates, CMA countries October 2023, (Eswatini inflation rate August 2023)

Source: Respective Central Banks, Respective Statistics Agencies & HEI Research

Our outlook is that the Bank of Namibia’s MPC will keep the repo rate unchanged at 7.75% to continue protecting the currency peg and to control inflation for price stability. We expect the interest rate pause to persist in the short term with possible cuts in the late first half of 2024.

In September 2023, national occupancy rates in Namibia stood at 65% a decline from 69% recorded in August 2023 (see Figure 1). This translated into a 4% monthly decline. When examining regional data, the northern region of the country achieved the highest occupancy rate at 68.9% for September 2023, followed by the central region at 66%. The coastal region reported the lowest occupancy rate for the second consecutive month at 57.8%. The surge in occupancy rates in the northern region could be attributed to the World Skills competition held in September, which could have attracted a significant influx of visitors, leading to heightened demand for accommodation facilities in the northern part of the country.

Furthermore, quarter 3 recorded a National occupancy rate of 65% an increase from 54.6% compared to quarter 3 last year and slightly higher than 64.7% recorded in 2019 pre-Covid. The Hospitality Association of Namibia attributed this growth primarily to a rise in arrivals from Central Europe. Both the German-speaking countries (D.A.CH) and France and Italy experienced increases of over 3% compared to 2019 levels. (See Figure 2).

The primary driver of these rates in Namibia remains leisure tourism. During the period under review, leisure-related occupancy rates constituted a substantial 88.7% of the total national occupancy rates, marking a decline from the 95.06% % recorded in August 2023.

Conversely, the business travel segment accounted for a 10% increase from 4.13% of the national occupancy rates recorded in August 2023. This signal improved business-related tourism activities.

The domestic market contributed 17.5% to the national occupancy during the review month, representing an increase from 14.22% recorded in August 2023. The decline indicates improved demand for domestic accommodation services. Most of the national occupancy was attributed to international tourists, with a substantial demand for occupancy originating from countries such as Germany, Switzerland, and Australia, accounting for 40.4% of international occupancy demand. This indicates a trend of reduced spending by locals on accommodation services.

Figure 1: National Occupancy Rates, Namibia (September 2022- September 2023)

Source: H.A.N & HEI RESEARCH

Figure 2: National Occupancy Rates, Namibia (Q3 2023 vs 2019(pre-Covid) & 2022(post-Covid)

Source: H.A.N & HEI RESEARCH

Outlook

As the country approaches the festive season, with holiday packages and specials expected to be announced soon, we anticipate the tourism sector to maintain its favorable trajectory in the short to medium term. Top of Form

During September 2023, new vehicle sales experienced a month-on-month decline of 3.7%, marking the third consecutive monthly decrease. A total of 1054 vehicles were sold in September 2023, compared to the 1094 vehicles sold in August 2023, reflecting a reduction of 40 vehicles. (Figure 1)

On an annual basis, vehicle sales increased by 3.5% when compared to September 2022. (Figure 1)

Month-on-month sales of passenger, medium commercial, and heavy commercial vehicles increased by 5%, 21%, and 86% while light commercial and extra heavy vehicles declined by 9% and 44% respectively.

During the first 9 months of 2023, 9842 vehicles were sold, comprising 4318 passenger vehicles, 4002 light commercial vehicles, 198 medium vehicles, 117 heavy commercial vehicles, 212 extra heavy commercial vehicles, and 12 buses. This resulted in a 20% annual growth compared to the corresponding period in the first nine months of 2022

Analysis

A 20% annual growth in new vehicles sold is an indication of overall improvement in consumer confidence

The continuous decline in monthly vehicle sales since June 2023 could be primarily attributed to diminished credit demand due to high interest rates and eroded disposable income

The rise in passenger vehicles could be due to no interest rate hike at the last Bank of Namibia’s MPC meeting. Consumers perceived this decision favorably, encouraging them to continue obtaining credit to purchase new cars

Sales of light commercial vehicles could be attributed to subdued commercial activities hence a low demand for commercial transportation services

Medium, heavy, and extra-heavy commercial vehicles continued on an upward trajectory. This could be mainly underpinned by the strong mining activity

The total sales of commercial vehicles experienced an 11% decline in September 2023, compared to the 590 units recorded in August 2023. This downturn underscores the suboptimal performance of the commercial sector

Table 1: Monthly vehicle sales by type

Market

Aug-23

Sep-23

Monthly unit change

Monthly % change

Passenger vehicles

502

528

26

5

Light commercial vehicles

505

458

-47

-9

Medium commercial vehicle sales

14

17

3

21

Heavy commercial vehicle sales

7

13

6

86

Extra heavy commercial vehicle sales

64

36

-28

-44

Bus

2

2

0

0

Figure 1: Monthly Vehicle Sales (September 2023 vs August 2023)

Source: Lightstone Auto & HEI RESEARCH

Figure 2: Year on Year, Vehicle Sales Growth (September 2022- September 2023)

Source: Lightstone (Pty) Ltd & HEI RESEARCH

Outlook

The demand for new vehicles has exhibited resilience despite prevailing high-interest rates. Looking ahead, we anticipate a continued month-on-month decline in vehicle sales in the short to medium term. However, the expectation could be influenced otherwise by the upcoming Bank of Namibia's Monetary Policy Committee's decision on the 25th of October 2023.

In September 2023, the annual inflation rate slowed to 5.4% compared to 7.1% in September 2022. (Figure 1)

The main contributors to a decline in the annual inflation were: transport, furnishings, household equipment, and routine maintenance of the houses and hotels, cafes, and restaurants, (Figure 2)

On a monthly basis, Namibia recorded an inflation rate of 0.8% an increase from 0.4% recorded for August 2023. The increase mainly emanated from the categories of transport (from 0.5 % to 2.9%), alcoholic beverages and tobacco (from 0.5% to 0.8%)

Analysis

The transport category which accounts for 14.3% of the consumer basket registered a decline in the annual inflation rate of 2.2% in August 2023 compared to 19.5% recorded in August 2022. The decline in the annual inflation rate for this component was reflected mainly in the subcomponent of operation of personal transport equipment which declined to 0.1% compared to 30% recorded in September 2022 attributed to a 3.3% fall in petrol and diesel prices

The annual inflation rate for furnishings, household equipment, and routine maintenance of the house which accounts for 5.5% of the consumer basket registered a decline in the annual inflation rate of 5.5% in September 2023 compared to 9.4% recorded in September 2022. This was attributed to a decline in the price levels of goods and services for routine household maintenance which declined to 4.5% compared to 25.1% recorded in September 2022

Hotels, cafes, and restaurants account for 1.4% of the consumer basket recorded a decline in the annual inflation rate of 6.9% in September 2023 compared to 11% recorded in September 2022. This was driven by a downturn in demand for accommodation services which declined to 7.6% compared to 20.4% recorded in September 2022.

Core inflation stood at 4.9% in September 2023 unchanged from 4.9% recorded in August 2023 and headline inflation increased to 5.4% for September 2023 from 4.7% recorded the previous month. The gap between core and headline inflation could raise concerns about long-term inflation trends. If this gap widens, it may signal a need for more proactive inflation-fighting measures. Figure 1

Figure 2: Sub-Categorical analysis (%) change Year on Year (September 2022 – September 2023)

Source: NSA & HEI Research

Outlook

The annual inflation for Namibia indicates a decreasing trend, driven by significant declines in specific categories such as transport and household expenses. The hospitality sector which is used as a proxy for the tourism sector also saw a reduction in inflation due to decreased demand for accommodation services. However, the gap between core and headline inflation raises concerns and calls for vigilant monitoring by the monetary and fiscal authorities to ensure price stability. We anticipate inflation to increase for the transport component due to higher Brent crude oil prices.

The agriculture, fishing, and forestry sector in Namibia remains crucial for reducing poverty, creating jobs, and making sure there is enough food. In 2022, real value added for ‘agriculture, fishing, and forestry’ recorded a growth of 2.6% when compared to a growth of 1.3% noted in the previous year. Livestock farming and ‘fishing and fish processing on board’ were the main drivers in the sector with improved growth rates of 1.2% and 2.3% during 2022 compared to a negative growth of 3.6% and a positive growth of 1.9% registered in the preceding year, respectively.

Analysis

The country’s export earnings from commodities in the agriculture, forestry, and fishing sectors amounted to N$ 6.2 billion whereas the import bill stood at N$ 3.4 billion. Fish products brought in N$4.1 billion in Q2 2023, up from N$3.2 billion in Q2 2022. However, the cost of importing fish products in the same period decreased to N$173.3 million from N$274.1 million in 2022. This translated into a 36.8 monthly decline.

Fisheries Products

During the period under review, horse mackerel was the most commonly caught fish, with 44,548 metric tons landed. Hake came second with 33,816 metric tons, and Monk was third with 1,825 metric tons. In Q2 2023, N$4.1 billion worth of fish and aquatic creatures were exported, compared to N$3.2 billion in Q2 2022. Spain was the top destination for these products, accounting for 36.6% of exports (mostly frozen hake fillets), followed by the Democratic Republic of Congo at 15.4% (mostly frozen mackerel), and Zambia at 14.3% (mostly horse mackerel).

Imports of fish and aquatic creatures were valued at N$173.3 million in Q2 2023, down from N$274.1 million in Q2 2022. These products mainly came from the Falkland Islands (mostly frozen cuttlefish and squid) at 65.8%, South Africa (mostly hake) at 20.2%, and Spain (mostly sardines) at 4.5%.

Livestock Auction

The total number of animals auctioned increased by 2.3% to 79,113 in Q2 2023 compared to 77,338 in the same quarter of 2022. Goats and cattle saw growth of 18.4% (18,933 more animals) and 6.1% (50,794 more animals), respectively. Sheep, on the other hand, declined from 13,482 in Q2 2022 to 9,386 in the current quarter. Prices for all types of livestock decreased during this period compared to the same quarter in 2022. Cattle prices dropped by 20.0% (N$25.96), while goat and sheep prices decreased by 17.4% (N$30.69) and 14.6% (N$28.70), respectively.

Trade of Selected Horticultural Products

In Q2 2023, dates were the top earners in horticultural product exports, bringing in N$25.8 million. Tomatoes and vegetable seeds followed with N$3.3 million and N$1.4 million, respectively. For imports, potatoes were the most significant, costing N$17.2 million in Q2 2023. Apples and onions came second and third, with import costs of N$8.7 million and N$7.0 million, respectively.

Figure 1: Agriculture, forestry, and fishing sector % share to GDP, (2022Q2 – 2023Q2)

Credit extended to households and businesses in the private sector marginally increased by N$59 million between July and August 2023. In monetary terms, total credit extended to the private sector grew from N$119,229.8 million in July 2023 to N$119,288.8 million in August 2023, due to the slight increase in demand for mortgages for households by 3.1% as well as installments and leasing credit by businesses by 17.7%.

On an annual basis, the Private Sector Credit Extension (PSCE) decelerated at 2.7%, from a 3.9% growth rate recorded at the end of July 2023 as debt obligations hinder consumers from taking up more credit facilities. (Figure 1). Furthermore, business credit contracted by 2.0% y/y, while household credit stood at 5.4% y/y.

Figure 1: Annual % PSCE vs. Repo Rate & Interest Rate, (January 2019- August 2023)

Source: BON, NSA & HEI RESEARCH

Credit to Households

The subdued growth in credit extended to households was driven by the sub-categories of; mortgage loans (from -2.9% to 3.1% m/m), while installment and leasing remained unchanged at 6.1% m/m (Figures 2&3). Additionally, there were declines in most credit facilities available to households, leading to minor overall growth. This was primarily attributed to a decrease in the uptake of weak overdraft credit, falling from 6.1% to 3.5%, and a decline in other loans and advances from 15.9% to 14.9% during the specified period (Refer to Figures 4 and 5)

Figure 2: Mortgage, (January 2021- August 2023)

Source: BON, NSA & HEI RESEARCH

Figure 3: Instalments and Leasing, (January 2021- August 2023)

Source: BON, NSA & HEI RESEARCH

Figure 4:, Overdrafts (January 2021- August 2023)

Source: BON, NSA & HEI RESEARCH

Figure 5: Other loans and advances, (January 2021- August 2023)

Source: BON, NSA & HEI RESEARCH

Credit to Businesses

The tightening in credit extended to businesses was driven by debt by businesses specifically in the services, wholesale and retail, commercial real estate, fishing as well as the transport sectors in the form of overdraft credit (from 6.8% to -0.4%), other loans and advances (from –6.6% to -5.5% m/m), and mortgage credit (from -5.1 to -4.4m/m) as illustrated in figure 5, 6 and 7. Furthermore, the demand for installments and leasing slightly improved from 16.6% to 17.7% m/m (Figure 8).

Figure 5: Overdrafts, (January 2021- August 2023)

Source: BON, NSA & HEI RESEARCH

Figure 6: Other loans and advances, (January 2021- August 2023)

Source: BON, NSA & HEI RESEARCH

Figure 7: Mortgage, (January 2021- August 2023)

Source: BON, NSA & HEI RESEARCH

Figure 8: Instalments and Leasing, (January 2021- August 2023)

Source: BON, NSA & HEI RESEARCH

Commercial Bank Liquidity Position

The overall liquidity position of the banking industry averaged N$8.9 billion in August 2023, depicting a month-on-month increase of N$26.1 million when compared to July 2023 (Figure 9). According to the Bank of Namibia (BoN), the increase was due to the rise in government payments as well as diamond sale proceeds.

Figure 9: Banking Liquidity (January 2021- August 2023)

Source: BON, NSA & HEI RESEARCH

Foreign Reserves & Money Supply

The Bank of Namibia’s stock of international reserves increased to N$55.6 billion in August 2023 from N$54.2 billion recorded in July 2023. The growth was attributed to the increase in commercial bank inflows, placements of Customer Foreign Currency (CFC), and gains from revaluation (Figure 10). Subsequently, growth in broad money supply significantly increased to 9.6 % in August 2023, from the 3.2% experienced in July 2023 (Figure 11).

Figure 10: Foreign Reserves (March 2020- August 2023)

The persistent weak demand for credit, particularly in business sectors such as overdrafts, mortgages, and other loans and advances, could suggest hesitancy among businesses to pursue credit due to a perceived lack of profitable investment opportunities. This hesitancy stems from a lack of confidence in their ability to generate future cash flows that would justify borrowing.

Conversely, the increasing trend in installments and leasing indicates a different scenario. Businesses opting for these financing options might be displaying greater confidence in their future revenue streams, indicating a willingness to invest in assets. This uptick reflects a belief in the profitability of such investments.

Similarly, the positive trend in credit demand from households, specifically in the mortgages and installment and leasing categories, mirrors consumer confidence in their financial future. The readiness of households to commit to long-term debt obligations underscores their positive outlook on income stability.

Considering these factors, we anticipate the Private Sector Credit Extension, particularly in the business category, to remain weak in the short to medium term. This projection is grounded in the cautious approach exhibited by both businesses and households, emphasizing the importance of economic stability and confidence in shaping credit market dynamics.